Identify your expenses and know where your money is going

In this installment of Money Tips, we’re going to show you how to identify where your money is going.

This will do two things:

- It will save you money right now by allowing you to immediately cancel those debits that aren’t necessary.

- It will set the foundation for future tips in which we will use this new-found knowledge to build our budget, track our spend and negotiate better rates on utilities, loans and other services.

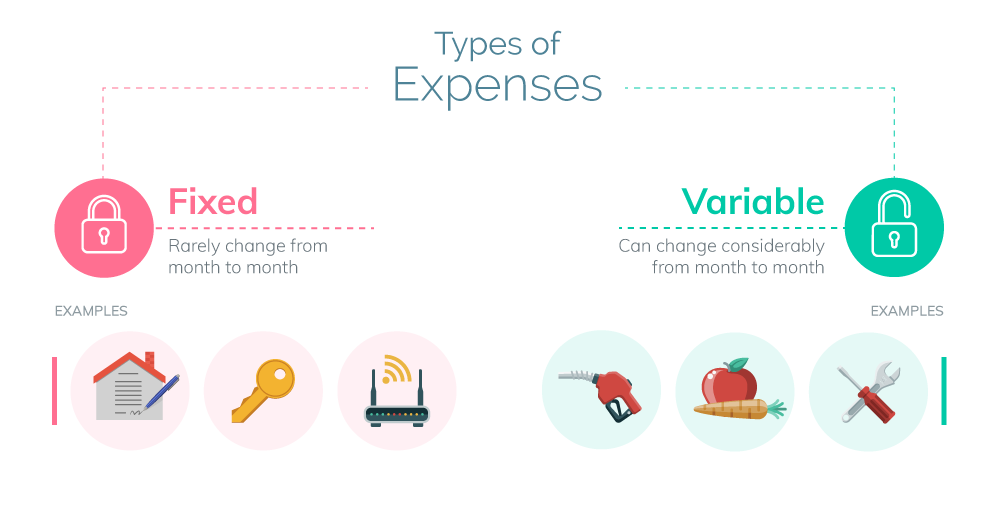

Types of expenses

Your expenses can largely be broken down into two categories: fixed or committed expenses and variable expenses.

Fixed expenses.

These are expenses that rarely change from month to month or quarter to quarter. They include rent, mortgage payments, credit card bills, internet, streaming services, council fees and so on. These are expenses you have committed to pay unless you cancel or change. You might even think of these as your bills.

Variable expenses.

These are your expenses where the amount may change from week to week or month to month and in some cases, are unexpected. Examples are groceries, medical bills, car repairs, pet costs, petrol, etc.

List your expenses

List all of your expenses into a column and next to each one, write fixed or variable. Then for each fixed expense, write down how much you pay per month, fortnight or quarter.

It will be difficult to come up with a figure for your variable expenses unless you’ve already tracked them over the course of several months.

Not to worry, for now all we’re trying to do is identify where your money is going – not necessarily how much is going there.

Don’t leave anything out

It’s easy to overlook certain expenses, especially direct debits and expenses that come up sporadically like birthday and Christmas gifts.

So really spend a lot of time on your list and consider all manner of expenses. Here are some ideas:

Not everyone will have the same categories so feel free to make your list suit you. For example, if you don’t often take prescription medication, you might lump prescriptions under “medical expenses” and label the whole lot as a variable expense.

On the other hand, if you regularly take a specific medication, it might make more sense to have a separate category called “regular prescriptions” and label that component as a fixed expense.

Ways to recognise a recurring expense

Here are some other ways to identify expenses that may be lurking somewhere in the depths of your accounts.

Check your recurring payments in PayPal

You know how a lot of subscription services will let you pay with PayPal? If you choose this route, PayPal will conveniently save all of your subscriptions in one place – to monitor, or even cancel, at your leisure.

But the list is a little hard to find so here’s how to find it (you can only do this on the desktop version of PayPal):

- Log into PayPal and click on the little gear icon in the top right corner of your screen.

- Click on “Payments”, which will appear in a second horizontal menu below the main menu.

- Click on the button in the middle of the page that says “Manage Automatic Payments”. Now all of your recurring PayPal payments will be listed on the far left of the page.

- From the list on the left, select “active subscriptions” to see only those subscriptions that have the potential to drain your accounts. We say “potential”, because it’s possible that not all of these “active” accounts are technically inactive. For example, if you cancelled your subscription directly through the service instead of PayPal.

- Click into any one of those subscriptions and see a list of most recent payments to any one of those services – this will help you identify whether you are still making payments.

Go through that list and identify any non-essential services that you can cut. As long as you are not bound by the terms of your agreement with the service to maintain your subscription for a certain length of time, you can take the axe to it right then and there.

Simply click on the subscription in question, and when the subscription details pop up on the right side of the page, click the button that says “cancel”.

Check your bank’s online portal for a list of direct debits

The term direct debit has become a catch-all term for automated payments, but there are actually two ways to set one up

- Traditional direct debit. This is when you authorise a third-party’s bank to take regular payments from your savings or transaction account to a third-party or another account you own. You organise this through your bank.

- Continuous payment authority (CPA). This is when you give your credit card or debit card details to a third-party, authorising them to charge your account on a regular basis. You set this up through the third party.

Your bank will have a list of all your traditional direct debits and you can usually access this through your bank’s online portal. Check there or give your bank a ring to access this list.

If you discover a direct debit that is safe to cancel (ie, you’re not under contract), then ask your bank to cancel the payments.

Work out the rest

Unfortunately, your bank won’t have a list of your active CPAs and you’ll have to work these out manually. Here are some tips.

- Make a list of all your utilities: phone, internet, electricity, gas, etc.

- Make a list of your health and life insurances

- Make a list of professional and social organisations and clubs you belong to

- Make a list of all the digital subscriptions you own: Netflix, Spotify, online video courses, Amazon Prime, meal deliveries, dating apps …

- Check your credit and debit card statements and highlight any other recurring payments

Go through this list and identify how you’re paying for each service. Many of these will be charged to your debit or credit card.

If you see any that are safe to cancel, call up the service provider and deliver the bad news. Or log into their online portal and cancel that way, if they offer the functionality.

With more and more services turning to a subscription-based model, it’s easy to lose track of everything you’ve signed up for.

So going forward, you might want to consider channeling future direct debits into one or two manageable places. For example, by using PayPal or your bank’s traditional direct debiting system.

In other words, avoid the Continuous Payment Authority (CPA) model where you give away your credit or debit card information one-by-one to service providers.

If you can’t avoid using CPAs, keep a list of every direct debit you set up this way.

What’s next?

After completing this exercise, you should have a better understanding of the nature of all your bills, expenses and debt obligations.

You should also know how much your fixed expenses are costing you, and hopefully you fattened your pockets some by closing a few unnecessary subscriptions.

In a future post, you will learn how to fill in some of the gaps in your expenses – namely how much your variable expenses are costing you. Since these fluctuate month-to-month, quarter-to-quarter and year-to-year, it takes a little more effort to identify what can actually be defined as a recurring expense and to arrive at a number.

To do this you’ll need to track your spend (for example with a handy spend tracking app) over the course of several months and then work out how much you spend on average each month.

But that takes us into budgeting territory, which is a whole topic on it’s own. So for now, just rejoice in the fact that you’ve gotten a leg up on your bills/subscriptions and gotten yourself into a money saving mindset.

That’s the name of the game.

The information in this blog post is general in nature and does not constitute personal financial or professional advice. It is not intended to address the circumstances of any particular individual or business. We do not guarantee the accuracy and completeness of the information and you should not rely on it. Before making any decisions, it is important for you to consider your personal situation, make independent enquiries and seek appropriate tax, legal and other professional advice.